Here’s a stat that surprised many operators when they first hear it:

The average cost to replace a loan officer who leaves is around $42,000. That includes recruiting costs, ramp time, lost production during transition, and training investment.

If your team loses 2 to 3 producers per year due to commission-related frustration (pay delays, calculation errors, lack of transparency), that adds up to $84,000 to $126,000 in replacement costs alone.

In our work with mortgage operations teams, those who implemented real-time commission visibility using Sequifi saw producer retention improve by an average of 35% year over year. That improvement leads directly to stronger financials: fewer replacement costs, less recruiting spend, and more stable production.

Here’s a breakdown of how this impact was measured, why it matters, and how mortgage teams can apply the same model.

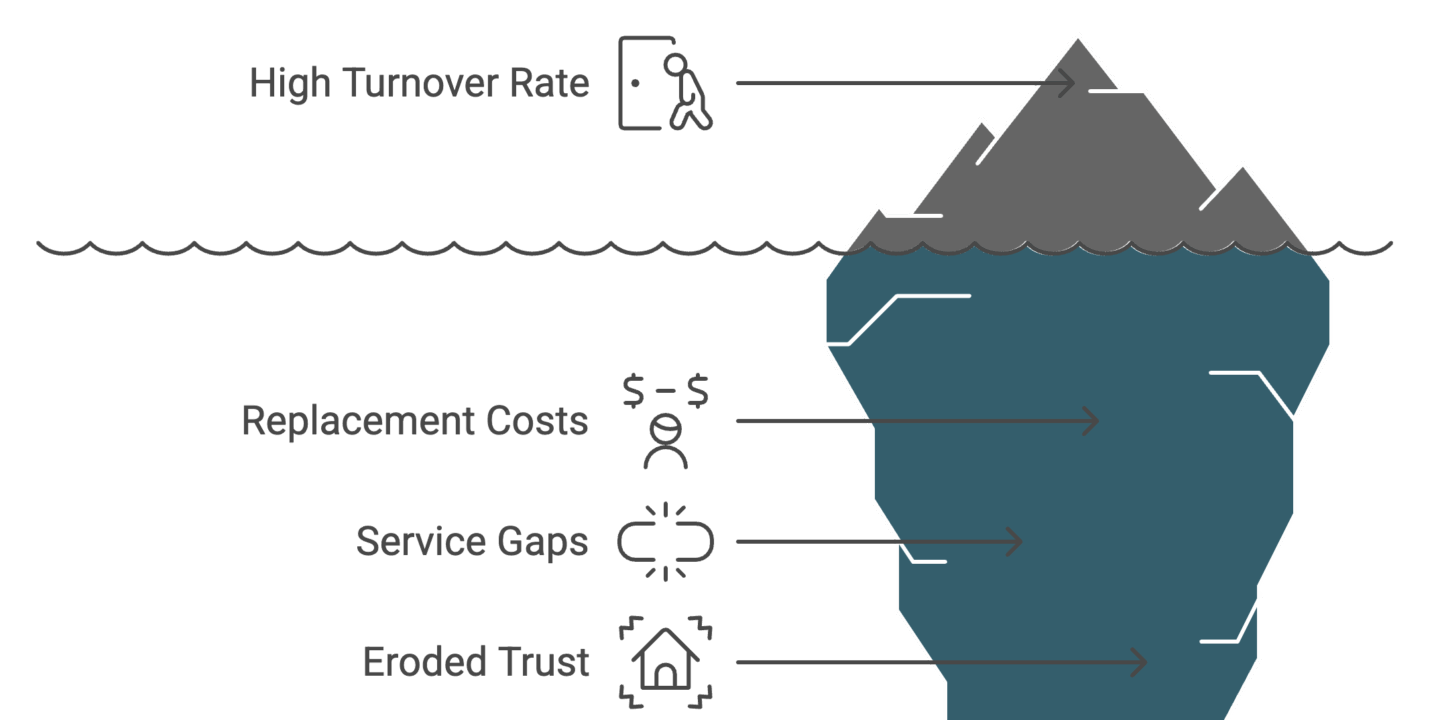

Why retention should be a top priority

Turnover among loan officers is a persistent and expensive challenge. For example:

- Industry data shows annual turnover rates for mortgage loan officers can average around 32% with an average tenure of about 3.9 years (Polygon Research).

- The cost of replacing a producing loan officer includes recruiting fees, signing bonuses, ramp time, onboarding, and the lost value of client relationships (National Mortgage News).

- From the borrower’s perspective, frequent LO changes can create service gaps, erode trust, and hurt repeat/referral business (Polygon Research).

When a loan officer leaves, the team loses more than a person. It loses pipeline momentum, relationship equity, and operational consistency.

Modeling the financial impact

By improving retention by 35%, what does that actually mean financially?

Example:

- A team has 40 producing loan officers.

- Historically, they lose 3 producers per year due to pay-related issues.

- At $42,000 per replacement, that’s $126,000 annually.

- With 35% improvement, the team would retain about one more LO per year.

- Replacement cost drops to $84,000.

- Savings: $42,000 annually.

This doesn’t even include gains in production stability or the avoided disruption to referral sources and pipeline flow.

How mortgage teams measured retention improvements

- Establish a baseline

- Total number of producing loan officers.

- Annual attrition rate of producers.

- Average cost to replace each one.

- Number of compensation disputes, pay delays, or manual override corrections.

- Introduce transparency and automation

- Use Sequifi to give LOs a real-time dashboard showing commission accruals, payout status, and exceptions.

- Automate commission logic to reduce errors.

- Surface any discrepancies clearly so they can be resolved before payout.

- Measure year over year changes

- Compare attrition against the previous year.

- Track reduced hiring/replacement spend.

- Monitor qualitative feedback from loan officers.

- Link to business outcomes

- Lower recruiting costs.

- More consistent production.

- Higher team morale and trust.

- Fewer service disruptions for borrowers.

Why commission visibility drives retention

Standard retention programs often miss the mark because they focus on high-level culture or perks rather than day-to-day trust. The most common frustration LOs voice is this: “I don’t know if I’m getting paid correctly or on time.”

Real-time visibility solves that. Here’s how:

- Builds trust: LOs can see how their pay is calculated and when to expect it.

- Reduces churn triggers: Errors, clawbacks, and delays drive producers to leave. Visibility prevents that.

- Improves focus: LOs spend more time originating and less time chasing numbers.

- Signals operational strength: Top producers are drawn to companies with modern systems. Clean pay ops signal a serious, growth-ready organization.

Steps to apply this model

- Audit your current attrition and costs

- How many producing LOs did you lose in the past 12 months?

- What was the cost per replacement?

- How many compensation-related disputes or delays occurred?

- Set measurable goals

- Target a 25 to 35% reduction in attrition.

- Model the cost savings from each retained LO.

- Implement visibility and automation

- Deploy real-time dashboards for LO compensation tracking.

- Automate the commission logic to reduce errors and delays.

- Track and communicate improvements

- Compare attrition trends quarterly and annually.

- Share retention wins with the team to reinforce the value of trust-driven operations.

Bottom line

Retention is not just a people problem. It is a profit lever. The cost of losing producing loan officers is too high to ignore, especially when most of the friction comes from outdated compensation workflows.

Real-time commission visibility, powered by automation, keeps your producers focused, your pipeline stable, and your recruiting budget under control.

If retention is a concern in your mortgage operation, it is time to put your pay process at the center of the conversation.